Note: To solve the heterogeneous agents model without aggregate risk, see my post on the Aiyagari model here.

Aiyagari type models can induce agents to save more than models with complete markets, however the level of savings is still much smaller than what we see in the data. While you can increase the savings rate by assuming larger values of risk aversion or income variability, there is little justification for these higher values. As Aiyagari writes,

“The quantitative results of this paper suggest that the contribution of uninsured idiosyncratic risk to aggregate saving is quite modest, at least for moderate and empirically plausible values of risk aversion, variability, and persistence in earnings.”

One possible explanation for the counterfactually low savings rate is that the standard Aiyagari model has no aggregate risk. The level of aggregate capital is known each period, resulting in a constant interest rate and wage. This implies that the only uncertainty that a consumer will face is with respect to their income process. It could be that adding in aggregate risk will make agents save even more, pushing up the aggregate savings rate and allowing us to better match the data.

Aiyagari excluded aggregate risk because it makes the problem far less tractable. Agents would need to not only forecast their individual state but also the distribution of assets in the economy (as that is what will determine prices in the subsequent period). But solving for a law of motion that moves any initial distribution forward one period and that is consistent with the optimal policy function is a daunting task. In their 1998 paper, “Income and Wealth Heterogeneity in the Macroeconomy,” Krusell and Smith (KS from now on) proposed a way to work around this problem and include aggregate risk. Rather than try and parameterize a transition function for the entire distribution, they assume that agents are boundedly rational and instead forecast moments of the distribution instead. Specifically, in their original paper, agents forecast the average level of capital

and assume that prices are determined by

where

Model Set-up and Parameterization

As is traditional in economic papers, we will be changing our baseline model slightly but will be changing the notation completely. For instance, Aiyagari writes

where utility is given by

Here,

The parameters that KS used to calibrate their model are given below. Note that

β = 0.99 δ = 0.025 α = 0.36 σ = 1.00000 hfix = 0.3271 # Hours worked homeY = 0.07 # The unemployment benefit

Aggregate prices are determined by a Cobb-Douglas production function

where

KS choose the probabilities to imply an unemployment rate of 4% in high states and 10% in low states. Let

That is, the measure of unemployed agent’s next period is the probability of an unemployed agent being unemployed, times the measure of unemployed agents, plus the probability of an employed worker becoming unemployed, times the measure of employed workers. An equivalent formula must hold for the measure of employed workers. These have to hold for any aggregate state transition (e.g. low to low or high to low).

Of course, these restrictions alone are not sufficient to pin down the transition matrix. KS therefore impose a few additional restrictions. First, the average duration of an unemployment spell is

and for bad states

To see this, note that the probability of not getting a job in

![E[\text{dur}] = \sum_{t=0}^{\infty} t \pi_{gg00}^t = \frac{1}{1-\pi_{gg00}}](https://s0.wp.com/latex.php?latex=E%5B%5Ctext%7Bdur%7D%5D+%3D+%5Csum_%7Bt%3D0%7D%5E%7B%5Cinfty%7D+t+%5Cpi_%7Bgg00%7D%5Et+%3D+%5Cfrac%7B1%7D%7B1-%5Cpi_%7Bgg00%7D%7D++&bg=ffffff&fg=73757D&s=0&c=20201002)

KS further impose

and

for reasons. The following code is largely lifted from the KS backup, although I changed some of the notation so that it is more consistent with their original paper.

urate = [0.1, 0.04, 0.1, 0.04]

durug = 1.5

unempg = 0.04

durgd = 8.0

durbd = 8.0

durub=2.5

unempb=0.1

πgg00 = (durug-1.0)/durug

πbb00 = (durub - 1.0)/durub

πbg00 = 1.25 * πbb00

πgb00 = 0.75 * πgg00

πgg01 = (unempg - unempg*πgg00)/(1.0-unempg)

πbb01 = (unempb - unempb*πbb00)/(1.0-unempb)

πbg01 = (unempb - unempg*πbg00)/(1.0-unempg)

πgb01 = (unempg - unempb*πgb00)/(1.0-unempb)

πgg = (durgd-1.0)/durgd

πgb = 1.0 - (durbd-1.0)/durbd

πgg10 = 1.0 - (durug-1.0)/durug

πbb10 = 1.0 - (durub-1.0)/durub

πbg10 = 1.0 - 1.25*πbb00

πgb10 = 1.0 - 0.75*πgg00

πgg11 = 1.0 - (unempg - unempg*πgg00)/(1.0-unempg)

πbb11 = 1.0 - (unempb - unempb*πbb00)/(1.0-unempb)

πbg11 = 1.0 - (unempb - unempg*πbg00)/(1.0-unempg)

πgb11 = 1.0 - (unempg - unempb*πgb00)/(1.0-unempb)

πbg = 1.0 - (durgd-1.0)/durgd

πbb = (durbd-1.0)/durbd

P0 =[

πbb*πbb00 πgb*πgb00 πbb*πbb10 πgb*πgb10;

πbg*πbg00 πgg*πgg00 πbg*πbg10 πgg*πgg10;

πbb*πbb01 πgb*πgb01 πbb*πbb11 πgb*πgb11;

πbg*πbg01 πgg*πgg01 πbg*πbg11 πgg*πgg11

]

4×4 Array{Float64,2}:

0.525 0.03125 0.35 0.09375

0.09375 0.291667 0.03125 0.583333

0.0388889 0.00208333 0.836111 0.122917

0.00911458 0.0243056 0.115885 0.850694

As with any macro model, we need to define a grid over out state variables. The following code determines the grids over aggregate capital and cash-in-hand. KS observe that the policy functions are very flat in the aggregate capital dimension, so I use 6 grid point between 10 and 13. This choice comes from the benefit of foresight. Typically it is necessary to start with a wider grid, see where the aggregate capital tends to fall and then successively narrow the grid until you have a good approximation. The reported regression coefficients have implied steady-state values of aggregate capital for the low and high states of

I choose the grid over cash-in-hand analogously to my Aiyagari code. The lowest value is set to the cash-in-hand an unemployed worker with zero assets would have (KS assume that the agent gets a flow value of

# Matrix of state values. First column is the aggregate state,

# second column is the individual state

fullY =[0.99 0.0;

1.01 0.0;

0.99 1.0;

1.01 1.0];

# Grid over the aggregate state

āmin = 10.0

# Next to no curvature here, arbitrary maximum state size

āmax = 13.0

abargrid = collect(linspace(āmin, āmax, 6))

# Minimum potential wealth. KS assume agent's can earn 0.07 when unemployed

zmin = 0.07

# Max sustainable investment

kmax = (δ/fullY[2,1])^(1/((α-1)))

zmax = 1.01*kmax^α + (1-δ)*kmax

# Create grid over cash on hand. Add more points towards the origin

kgrid = collect(linspace(zmin^(1/30), zmax^(1/30), 50).^30)

# Maximum assets = cash-in-hand

maxa = zeros(length(kgrid), length(abargrid), 4)

for s = 1:4

as = kgrid *(abargrid'./abargrid')

maxa[:,:,s] = as - 0.001

end

Interpolation Object and Associated Functions

The interpolating object is more complicated than in the Aiyagari model, as we now need to keep track of both the aggregate state and a law of motion for this state. This requires adding a grid over aggregate capital and a grid for the distribution of assets. We also need to add regression coefficients which represent the agent’s best guess at the law of motion for aggregate capital. The below custom type stores all of the relevant variables.

# Interpolating Object

type GalerkinObj

β::Float64

δ::Float64

α::Float64

σ::Float64

ζ::Float64

ϕ::Float64

hfix::Float64 # Average Hours

homeY::Float64 # Home Production

urate::Array{Float64,1} # Unemployment rates in good and bad states

P::Array{Float64, 2} # Transition Matrix

reg::Array{Float64, 2} # Regression Coefficients

states::Array{Float64,2} # Potential States after shocks (both idiosyncratic and aggregate)

θs::Array{Float64, 3} # FEM coefficients

gridk::Array{Float64, 1} # Individual capital grid points

gridK::Array{Float64, 1} # Aggregate Capital grid points

agrid::Array{Float64, 1} # Distribution grid

Kdist::Array{Float64, 1} # Distribution of Capital

function GalerkinObj(β, δ, α, σ, ζ, ϕ, hfix, homeY, urate, P, reg, states, gridk, gridK, agrid)

return new(β, δ, α, σ, ζ, ϕ, hfix, homeY, urate, P, reg, states, zeros(length(gridk), length(gridK), length(states)),

gridk, gridK, agrid, zeros(length(agrid)*2))

end

end

# Grid for distribution

agrid = collect(linspace(0.0, zmax, 300));

# My custom type

go = GalerkinObj(β, δ, α, σ, 0.0, 0.0, hfix, 0.07, urate, P0, [0.085 0.095; 0.965 0.962], fullY, kgrid, abargrid, agrid);

go.θs = maxa*0.98;

Interpolation is carried out using bilinear interpolation. Each grid point has an associated coefficient in our interpolating object. Any sample point will fall in the middle of four grid points. The below function takes two coordinates, x and y, and does a simple sorted search over the grids for individual capital and aggregate capital and returns the index of the grid point immediately before the sample coordinate. Using the indices of these lower grid points and their immediate successors we can determine the four coefficients that contribute to our interpolated value. Wikipedia has a good discussion on bilinear interpolation and provides various methods for calculating an interpolated value (see here).

function(itp::GalerkinObj)(x::Float64, y::Float64, s::Int64)

gridx = itp.gridk

gridy = itp.gridK

indxl = min(max(searchsortedlast(gridx,x), 1), length(gridx)-1)

indyl = min(max(searchsortedlast(gridy,y), 1), length(gridy)-1)

yh = gridy[indyl+1];

yl = gridy[indyl];

xl = gridx[indxl];

xh = gridx[indxl + 1];

denom = (xh-xl)*(yh-yl)

a11 = itp.θs[indxl, indyl, s]

a12 = itp.θs[indxl, indyl+1, s]

a21 = itp.θs[indxl+1, indyl, s]

a22 = itp.θs[indxl+1, indyl+1, s]

return (a11*(xh - x)*(yh - y) + a21*(x - xl)*(yh - y) + a12 * (xh - x)*(y - yl) + a22*(x-xl)*(y-yl))/denom

end

We will need to take the derivative of this interpolation object with respect to both the interpolation coefficients and the various arguments. These are easy to calculate, and I wrap them in the following two functions.

# Derivative for specific coefficient

function(itp::GalerkinObj)(d1::Int64, d2::Int64, x::Float64, y::Float64, s::Int64)

gridx = itp.gridk

gridy = itp.gridK

indxl = min(max(searchsortedlast(gridx,x), 1), length(gridx)-1)

indyl = min(max(searchsortedlast(gridy,y), 1), length(gridy)-1)

yh = gridy[indyl+1];

yl = gridy[indyl];

xl = gridx[indxl];

xh = gridx[indxl + 1];

denom = (xh-xl)*(yh-yl)

if (d1 == indxl)&(d2 == indyl)

deriv = (xh - x)*(yh - y) / denom

elseif (d1 == indxl+1)&(d2 == indyl)

deriv = (x - xl)*(yh - y) / denom

elseif (d1 == indxl)&(d2 == indyl + 1)

deriv = (xh - x)*(y - yl) / denom

elseif (d1 == indxl+1)&(d2 == indyl+1)

deriv = (x-xl)*(y-yl) / denom

else

deriv = 0.0

end

return deriv

end

# Derivative for specific state

function(itp::GalerkinObj)(x::Float64, y::Float64, s::Int64, d::Int64)

gridx = itp.gridk

gridy = itp.gridK

indxl = min(max(searchsortedlast(gridx,x), 1), length(gridx)-1)

indyl = min(max(searchsortedlast(gridy,y), 1), length(gridy)-1)

yh = gridy[indyl+1];

yl = gridy[indyl];

xl = gridx[indxl];

xh = gridx[indxl + 1];

denom = (xh-xl)*(yh-yl)

a11 = itp.θs[indxl, indyl, s]

a12 = itp.θs[indxl, indyl+1, s]

a21 = itp.θs[indxl+1, indyl, s]

a22 = itp.θs[indxl+1, indyl+1, s]

if d == 1

deriv = (-a11*(yh - y) + a21*(yh - y) - a12*(y - yl) + a22*(y-yl))/denom

else

deriv = (-a11*(xh - x) - a21*(x - xl) + a12 * (xh - x) + a22*(x-xl))/denom

end

return deriv

end

The Euler Equation and its Derivative

The Euler Equation does not change much between our original Aiyagari model and the KS model. The primary difference is that

We again choose the coefficient in our finite element method to solve

where

Prices in the period will therefore be predicted to be

Using this wage and interest rate we can calculate the implied cash-in-hand next period and use our current guess at the savings policy function to calculate implied consumption and savings.

function R_all(z::Float64, abar::Float64, s::Int64, â::GalerkinObj)

ζ, σ, β, ϕ, δ, hfix, homeY, α, P, reg, urate = â.ζ, â.σ, â.β, â.ϕ, â.δ, â.hfix, â.homeY, â.α, â.P, â.reg, â.urate

ys = â.states

â′ = â(z, abar, s)

abar′ = exp(reg[1, mod(s+1, 2) + 1] + reg[2, mod(s+1, 2) + 1]*log(abar))

lhs = 0.0

rhs = (z - â′ )^(-σ) - ζ * min(â′, ϕ)^2

for s′ = 1:size(ys, 1)

r = α * ys[s′, 1] * (hfix*(1.0 - urate[s′])/abar′)^(1.0-α) - δ

w = (1-α) * ys[s′, 1] * (abar′/(hfix*(1.0 - urate[s′])))^(α)

z′s = w*ys[s′,2]*hfix + homeY*(1.0 - ys[s′,2]) + (1.0 + r)*â′ - r*ϕ

â′′ = â(z′s, abar′, s′ )

lhs += (1.0 + r)*(z′s - â′′)^(-σ)*P[s, s′]

end

lhs = β * lhs

return rhs - lhs

end

The derivative with respect to a given coefficient is straightforward to calculate as well. Each coefficient can be associated with an index

function R′_all(dz::Int64, dabar::Int64, ds::Int64, z::Float64, abar::Float64, s::Int64, â::GalerkinObj)

ζ, σ, β, ϕ, δ, hfix, homeY, α, P, reg, urate = â.ζ, â.σ, â.β, â.ϕ, â.δ, â.hfix, â.homeY, â.α, â.P, â.reg, â.urate

â_d = â(dz, dabar, z, abar, ds)

ys = â.states

â′ = â(z, abar, s)

abar′ = exp(reg[1, mod(s+1, 2) + 1] + reg[2, mod(s+1, 2) + 1]*log(abar))

rhs = σ*(z - â′ )^(-σ-1.0)*â_d*(ds==s) - ζ * 2.0 * min(â′, ϕ)*â_d*(ds==s)

lhs = 0.0

if ds == s

for s′ = 1:size(ys, 1)

r = α * ys[s′, 1] * (hfix*(1.0 - urate[s′])/abar′)^(1.0-α) - δ

w = (1-α) * ys[s′, 1] * (abar′/(hfix*(1.0 - urate[s′])))^(α)

z′s = w*ys[s′,2]*hfix + homeY*(1.0 - ys[s′,2]) + (1 + r)*â′ - r*ϕ

â′′ = â(z′s, abar′, s′ )

lhs += -(1+r)*σ*(z′s - â′′)^(-σ-1.0)*((1.0+r)*(â_d - â(z′s, abar′, s′, 1)*â_d) - â(dz, dabar, z′s, abar′, s′)*(s==s′)) * P[s, s′]

end

else

r = α * ys[ds, 1] * (hfix*(1.0 - urate[ds])/abar′)^(1-α) - δ

w = (1-α) * ys[ds, 1] * (abar′/(hfix*(1.0 - urate[ds])))^(α)

z′s = w*ys[ds,2]*hfix + homeY*(1.0 - ys[ds,2]) + (1 + r)*â′ - r*ϕ

lhs = -(1.0+r)σ*(z′s - â(z′s, abar′, ds))^(-σ-1.0)*( - â(dz, dabar, z′s, abar′, ds) ) * P[s, ds]

end

lhs = β*lhs

return rhs - lhs

end

One benefit of the Galerkin Method is that it leads to sparse Jacobians. This greatly reduces the computational cost of our Newton’s method, as we only need to calculate the values of a few specific elements in the matrix. Because we use bilinear interpolation, only four coefficients contribute to our interpolated value for any given point

Notice that the residual equation evaluates the policy function at

Quick computational note: For efficient code, the three steps that I just laid out – solving for the residual value, identifying non-zero elements in the Jacobian, and solving for the derivative – should all be combined in a single step. Note that many of the calculations that I have done (such as calculating the interest rate, or evaluating the policy function) are redundant. I break these steps out into individual functions for clarity, but ultimately this will not scale as well as a single piece of code where these steps are all combined.

function idcell2!(tmp::Array{Int64, 2}, z::Float64, abar::Float64, s::Int64, â::GalerkinObj)

ζ, σ, β, ϕ, δ, hfix, homeY, α, P, reg, urate = â.ζ, â.σ, â.β, â.ϕ, â.δ, â.hfix, â.homeY, â.α, â.P, â.reg, â.urate

ys = â.states

kgrid = â.gridk

Kgrid = â.gridK

count = 1

# grid on capital

idxz1 = min(max(searchsortedlast(kgrid, z), 1), length(kgrid)-1)

idxbar1 = min(max(searchsortedlast(Kgrid, abar), 1), length(Kgrid)-1)

abar′ = exp(reg[1, mod(s+1, 2) + 1] + reg[2, mod(s+1, 2) + 1]*log(abar))

idxbar2 = min(max(searchsortedlast(Kgrid, abar′), 1), length(Kgrid)-1)

# projected assets and state

â′ = â(z, abar, s)

for idz = idxz1:idxz1+1

for idbar = idxbar1:idxbar1+1

tmp[count, 1] = idz; tmp[count, 2] = idbar; tmp[count, 3] = s

count += 1

end

end

for idxbar = idxbar2:idxbar2+1

for s′ = 1:size(ys, 1)

r = α * ys[s′, 1] * (hfix*(1.0 - urate[s′])/abar′)^(1-α) - δ

w = (1-α) * ys[s′, 1] * (abar′/(hfix*(1.0 - urate[s′])))^(α)

z′s = w*ys[s′,2]*hfix + homeY*(1.0 - ys[s′,2]) + (1.0 + r)*â′ - r*ϕ

idxz2 = min(max(searchsortedlast(kgrid, z′s), 1), length(kgrid)-1)

for idxz′ = idxz2:idxz2+1

if (s′ == s)&(idxz′ == idxz1)&(idxbar == idxbar1)|

(s′ == s)&(idxz′ == idxz1+1)&(idxbar == idxbar1)|

(s′ == s)&(idxz′ == idxz1)&(idxbar == idxbar1+1)|

(s′ == s)&(idxz′ == idxz1+1)&(idxbar == idxbar1+1)

continue

else

tmp[count, 1] = idxz′; tmp[count, 2] = idxbar; tmp[count, 3] = s′

count += 1

end

end

end

end

return nothing

end

Weighted Residual and Newton’s Method

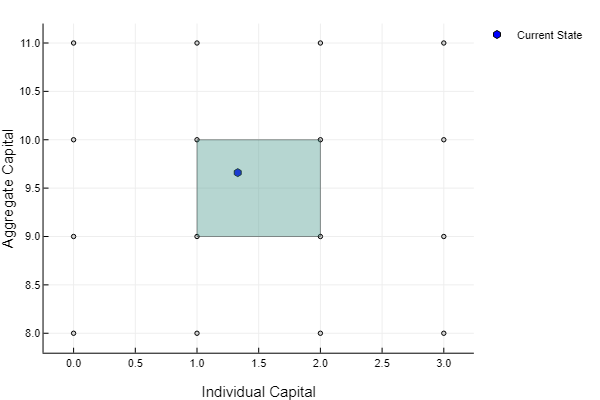

More care needs to be taken in two dimensions when constructing our weighted residual equation. Again, our weights are given by hat functions. Each hat function spans four individual elements (each different shade of green is an element in the image below). The hat function takes the value

The total number of elements is equal to the product of our grid dimensions, so by iterating over all grid points we will transverse all of the elements. The below code iterates over the states, the aggregate capital grid, and the individual capital grid and creates four indices at each step

idx1 = (s-1)*nk*nK + nk*(j-1) + i idx2 = (s-1)*nk*nK + nk*(j-1) + i + 1 idx3 = (s-1)*nk*nK + nk*(j) + i idx4 = (s-1)*nk*nK + nk*(j) + i + 1

These are linear indices that uniquely identify the four weighted residual equations that the current element contributes to. The function calculates the residual and its derivative at the four quadrature nodes, gives the values the appropriate weights, and then adds these values to the array position determined by the above indices. In this way, we build up the weighted residual values in a piece-wise fashion. I include four additional weights below, m1 – m4, which only serve to add more weight to the equations on the boundary. For instance, the weighted residual equations at the corners only have a single element contributing to their value, so I scale the calculated value by 4. All weighted residual equations will therefore have roughly 4 elements contributing to their value. I have found that this improved the stability of my Newton’s method.

function weightedResidual(go::GalerkinObj, N::Int64)

nodes, weights = gausslegendre(N)

resc1 = zeros(length(nodes))

resc2 = zeros(length(nodes))

w1 = zeros(length(nodes))

w2 = zeros(length(nodes))

Gθ = zeros(length(go.θs), length(go.θs))

res = zeros(length(go.θs))

tmp = zeros(Int64, size(go.states,1)*5, 3) # for check id of cells

nk = length(go.gridk)

nK = length(go.gridK)

foridx = size(go.θs)

eps = vec(go.θs); count = 0

while (maximum(abs(eps)) > 1e-10)*(40 > count)

count += 1

# Reset Values to zero

for i = 1:length(res)

res[i] = 0.0

for j = 1:length(res)

Gθ[i,j] = 0.0

end

end

# Iterate over states

for s = 1:size(go.states,1)

# iterate over grid points

for j = 1:nK-1

for i = 1:nk-1

kl = go.gridk[i] ; kh = go.gridk[i + 1];

Kl = go.gridK[j]; Kh = go.gridK[j+1];

denom = (kh - kl)*(Kh - Kl) # Denominator

for n = 1:length(nodes)

resc1[n] = (nodes[n]+1.0)*(kh-kl)/2.0 + kl

resc2[n] = (nodes[n]+1.0)*(Kh-Kl)/2.0 + Kl

w1[n] = weights[n]*(kh-kl)/2.0

w2[n] = weights[n]*(Kh-Kl)/2.0/denom

end

m1 = ifelse(i == 1, 2.0, 1.0)

m2 = ifelse(j == 1, 2.0, 1.0)

m3 = ifelse(i + 1 == nk, 2.0, 1.0)

m4 = ifelse(j + 1 == nK, 2.0, 1.0)

idx1 = (s-1)*nk*nK + nk*(j-1) + i

idx2 = (s-1)*nk*nK + nk*(j-1) + i + 1

idx3 = (s-1)*nk*nK + nk*(j) + i

idx4 = (s-1)*nk*nK + nk*(j) + i + 1

# Function

for k_ = 1:length(resc1)

for K_ = 1:length(resc2)

for tt = 1:length(tmp)

tmp[tt] = 0

end

val = R_all(resc1[k_], resc2[K_], s, go)

weigh = w1[k_]*w2[K_]

res[idx1] += weigh*val*(kh - resc1[k_])*(Kh - resc2[K_])*m1*m2

res[idx2] += weigh*val*(resc1[k_] - kl)*(Kh - resc2[K_])*m2*m3

res[idx3] += weigh*val*(kh - resc1[k_])*(resc2[K_]-Kl)*m1*m4

res[idx4] += weigh*val*(resc1[k_] - kl)*(resc2[K_] - Kl)*m3*m4

idcell2!(tmp, resc1[k_], resc2[K_], s, go)

# Derivative

for c = 1:size(tmp,1)

if tmp[c,1] != 0

gs = tmp[c,3]; gj = tmp[c,2]; gi = tmp[c,1]

idxd = (gs-1)*nk*nK + nk*(gj-1) + gi

val = R′_all(gi, gj, gs, resc1[k_], resc2[K_], s, go)

Gθ[idx1, idxd] += weigh*val*(kh - resc1[k_])*(Kh - resc2[K_])*m1*m2

Gθ[idx2, idxd] += weigh*val*(resc1[k_] - kl)*(Kh - resc2[K_])*m2*m3

Gθ[idx3, idxd] += weigh*val*(kh - resc1[k_])*(resc2[K_]-Kl)*m1*m4

Gθ[idx4, idxd] += weigh*val*(resc1[k_] - kl)*(resc2[K_] - Kl)*m3*m4

end

end

end

end

end

end

end

eps = -Gθ\res

for i = 1:length(go.θs)

go.θs[i] += eps[i]#*ifelse(count<5,0.5,1.0)

end

end

for i = 1:length(go.θs)

go.θs[i] = max(go.θs[i], 0.0)#*ifelse(count<5,0.5,1.0)

end

@show maximum(abs(eps))

return nothing

end

go = GalerkinObj(β, δ, α, σ, 0.0, 0.0, hfix, 0.07, urate, P0, [0.085 0.095; 0.965 0.962], fullY, kgrid, abargrid, agrid);

go.ζ = 1000000.0

go.θs = maxa*0.98;

@time weightedResidual(go, 2)

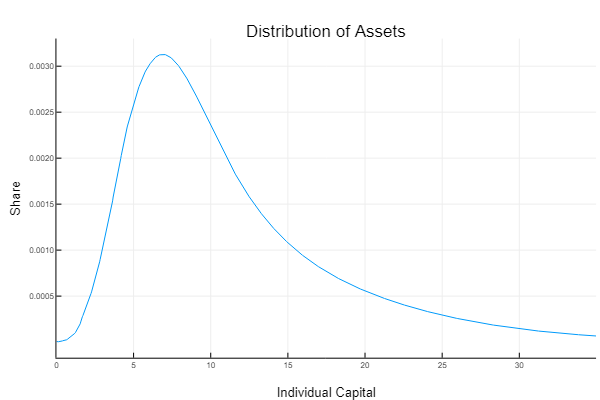

Calculating the Distribution of Assets

I again use Young’s histogram method to determine the distribution of assets. KS use simulation, which is slower and less accurate. A problem that KS faced was that simulation could not force the unemployment rate to be

function calcStatDist(â::GalerkinObj, K::Float64, s::Int64, s′::Int64, Φ::Array{Float64,2})

ζ, σ, β, ϕ, δ, hfix, homeY, α, P, reg, urate = â.ζ, â.σ, â.β, â.ϕ, â.δ, â.hfix, â.homeY, â.α, â.P, â.reg, â.urate

ys = â.states

agrid = â.agrid

Kdist = â.Kdist

# Interest rates

r = α * ys[s, 1] * (hfix*(1.0 - urate[s])/K)^(1-α) - δ

w = (1-α) * ys[s, 1] * (K/(hfix*(1.0 - urate[s])))^α

# Transition matrix, given states

z = ifelse(s == 1, [1,3], [2,4])

z′ = ifelse(s′ == 1, [1,3], [2,4])

P2 = P[z, z′]./sum(P[z, z′], 2)

# Reset to 0

for i = 1:length(Φ)

Φ[i] = 0.0

end

AM = size(Φ,1)

M = length(agrid)

for i = 1:AM

k = div(i-1, M)*2 + 1 + 1*(s == 2)

ss = div(i - 1, M) + 1

# Current capital point

a1 = ifelse(mod(i, M) == 0, M, mod(i, M))

# Implied asset holdings

z′s = w*ys[k,2]*hfix + homeY*(1.0 - ys[k,2]) + (1.0 + r)*agrid[a1] - r*ϕ

a′ = â(z′s, K, k)

indxL = searchsortedlast(agrid, a′)

indxL == 0 && return @show z′s, K

indxH = indxL + 1

if M > indxL

w1 = (agrid[indxH] - a′)/(agrid[indxH] - agrid[indxL])

w2 = (a′ - agrid[indxL])/(agrid[indxH] - agrid[indxL])

# If outside capital grid, then set to max

else

indxL = M-1

indxH = M

w1 = 0.0

w2 = 1.0

end

for j = 1:size(P2,1)

Φ[i,M*(j-1) + indxL] = P2[ss, j] * w1

Φ[i,M*(j-1) + indxH] = P2[ss, j] * w2

end

end

if sum(Kdist) == 0.0

return statDist = (eye(M*size(P2,1)) - Φ + ones(M*size(P2,1),M*size(P2,1)))'\ones(M*size(P2,1))

else

return Φ' * Kdist

end

end

Simulating the Economy and Estimating the Law of Motion

To simulate the data we take

tmp = hcat(P0[:,1]+P0[:,3], P0[:,2]+P0[:,4])

condP0 = hcat(tmp[1,:]+tmp[3,:], tmp[2,:]+tmp[4,:])

condP0 = condP0./sum(condP0,2)

conPsummed = cumsum(condP0,2)

T = 15000

aggs = rand(T)

indx = 2

aggsts = Int64[]

for i = 1:T

indx = searchsortedfirst(conPsummed[indx,:], aggs[i])

append!(aggsts, indx)

end

For the sake of efficiency, I create a custom type to store the regression objects. This will keep us from having to reallocate arrays for the dependent and independent variables.

type regObj

Φ::Array{Float64, 2}

aggsts::Array{Int64, 1}

aggK::Array{Float64, 1}

T::Int64

y::Array{Float64, 1}

x::Array{Float64, 2}

βs::Array{Float64, 1}

function regObj(Φ, aggsts)

return new(Φ, aggsts, zeros(aggsts), length(aggsts), zeros(length(aggsts)-1), zeros(length(aggsts)-1, 4), zeros(4))

end

end

Starting from our initial distribution of capital (chosen so that the average capital stock is approximately

function genCoeff(â::GalerkinObj, regobj::regObj)

agrid = â.agrid

fullgrid = vcat(agrid,agrid)

K = dot(â.Kdist, fullgrid)

Φ = regobj.Φ

aggsts = regobj.aggsts

aggK = regobj.aggK

####### Calculate the time series

regobj.aggK[1] = K

for i = 2:regobj.T

m0 = regobj.aggK[i-1]

s1 = aggsts[i-1]

s2 = aggsts[i]

â.Kdist = calcStatDist(â, m0, s1, s2, regobj.Φ)

m0 = dot(â.Kdist, fullgrid)

regobj.aggK[i] = m0

end

return nothing

end

KS recommends separating your data by state and then running individual regressions. This is the same as running a single regression with a dummy for each state and an interaction term between the state dummy and log aggregate capital. You need to throw out a number of observations at the beginning of your simulation to ensure that the estimates do not depend on your initial distribution of capital. I throw out the first

function regression(regobj::regObj)

for i = 1:length(regobj.y)

regobj.y[i] = log(regobj.aggK[i+1])

end

for i = 1:length(regobj.y)

regobj.x[i, 1] = 1.0

regobj.x[i, 2] = log(regobj.aggK[i])

regobj.x[i, 3] = 1.0 * (regobj.aggsts[i] == 2)

regobj.x[i, 4] = regobj.x[i, 2] * regobj.x[i, 3]

end

regobj.βs = (regobj.x[1500:end,:]'regobj.x[1500:end,:])\regobj.x[1500:end,:]'regobj.y[1500:end]

return nothing

end

Putting it all together

We can now combine each of these functions to create a “contraction” to find a fixed point of the regression coefficients. For each iteration we combine three steps. First, we solve for the optimal policy function using our weighted residual equation. Second, we simulate the economy from a starting distribution using our policy function and store our aggregate states. Finally, we regress future states on past states to generate an updated law of motion for the aggregate capital stock. Unfortunately this process is not a true contraction. In fact, if your grid is not fine enough in the histogram method then this process can still diverge even if your initial guess is very close to the fixed point. However, rather than increase the how fine your grid is, you can circumvent this issue by using a dampened step. Rather than updating your guess to the newly calculated regression coefficients, you use a convex combination of the old guess and the new estimates.

where

function contraction(â::GalerkinObj, regobj::regObj, qnodes::Int64, baseDist::Array{Float64, 1}, λ::Float64)

eps = 1.0

count = 0

while (eps > 1e-6)*(9 > count)

weightedResidual(â, qnodes)

for i = 1:length(â.Kdist)

â.Kdist[i] = baseDist[i]

end

genCoeff(â, regobj)

regression(regobj)

eps = 0.0

for i = 1:4

eps = max(eps, abs(â.reg[i] - regobj.βs[i] - regobj.βs[2-mod(i,2)]*(i > 2) ))

end

# reset coefficients

â.reg[1] = regobj.βs[1]*λ + (1-λ)*â.reg[1]

â.reg[2] = regobj.βs[2]*λ + (1-λ)*â.reg[2]

â.reg[3] = (regobj.βs[1] + regobj.βs[3])*λ + (1-λ)*â.reg[3]

â.reg[4] = (regobj.βs[2] + regobj.βs[4])*λ + (1-λ)*â.reg[4]

count += 1

@show eps

end

return nothing

end

Φ = zeros(2*length(agrid), 2*length(agrid)); regobj = regObj(Φ, aggsts); @time weightedResidual(go, 2) go.Kdist = zeros(go.Kdist) baseDist = calcStatDist(go, 11.6, 1, 2, regobj.Φ) @time contraction(go, regobj, 2, baseDist, 0.4)

maximum(abs(eps)) = 3.8030270272729575e-12 5.812602 seconds (348 allocations: 407.035 MB, 9.28% gc time) maximum(abs(eps)) = 2.9172414536690923e-12 maximum(abs(eps)) = 5.329161385265171e-12 maximum(abs(eps)) = 2.8452345649151584e-12 maximum(abs(eps)) = 6.61078433135063e-12 maximum(abs(eps)) = 6.77579338591743e-12 maximum(abs(eps)) = 6.022658600410299e-12 maximum(abs(eps)) = 4.456933600887884e-12 maximum(abs(eps)) = 4.3840564713644485e-12 maximum(abs(eps)) = 3.703572413541803e-12 eps = 1.2340961612844481e-5 107.143052 seconds (4.07 M allocations: 3.625 GB, 0.83% gc time)

I don’t recover the estimates in KS exactly as I use a coarser grid over my state space. However, the estimates are still very close, off by less than a percent.

go.reg

2×2 Array{Float64,2}:

0.0856849 0.0942881

0.964057 0.962587

Interestingly, it does not appear that the addition of aggregate shocks leads to a considerable improvement in the model’s performance. The aggregate savings rate increases a bit, but the distribution of assets is still very similar to what you generate in a basic Aiyagari type model. To get a more realistic distribution, KS add ex-ante heterogeneity to their agents. Rather than having agents with identical expected utility functions, they allow agents to have different discount rates, which leads to different propensities to save.

References

- Per Krusell & Anthony A. Smith & Jr., 1998. “Income and Wealth Heterogeneity in the Macroeconomy,” Journal of Political Economy, University of Chicago Press, vol. 106(5), pages 867-896, October.

- S. Rao Aiyagari, 1994. “Uninsured Idiosyncratic Risk and Aggregate Saving,” The Quarterly Journal of Economics, Oxford University Press, vol. 109(3), pages 659-684.

- Ellen R. McGrattan, 1993. “Solving the stochastic growth model with a finite element method,” Staff Report 164, Federal Reserve Bank of Minneapolis.

- Young, Eric R., 2010. “Solving the incomplete markets model with aggregate uncertainty using the Krusell-Smith algorithm and non-stochastic simulations,” Journal of Economic Dynamics and Control, Elsevier, vol. 34(1), pages 36-41, January.

In the published version of paper condition :

πbg00 = 1.25 * πbb00

πgb00 = 0.75 * πgg00

has been replaced by

Pi_{gb00}*Pi_{gb}^{-1}= 1.25 Pi_{bb00}*Pi_{bb}^{-1}

Pi_{bg00}*Pi_{bg}^{-1}= 0.75 Pi_{gg00}*Pi_{gg}^{-1}

LikeLike