Many important questions in economics require us to consider heterogeneous agent models. For instance, the standard representative agent model could not be used to study the distribution of wealth because, by definition, a single agent has all of the wealth. Possibly the most important paper in this literature is S. Rao Aiyagari’s 1994 paper “Uninsured Idiosyncratic Risk and Aggregate Saving”. Aiyagari considered an economy where all the agents were ex ante identical, but due to a random income process were ex post heterogeneous. Additionally, he considered agents that were borrowing constrained so that they would be incentivized to increase savings for precautionary reasons. The following code replicates some results from Aiygari’s original paper and can be extended to replicate all of his results. For the interested reader, Aiyagari’s 1993 paper (of the same name) has additional results and elaborates further on the algorithm that he used.

The Model

The defining characteristic of the Aiyagari model is that there is uninsured idiosyncratic risk. This risk manifests itself as a shock to each consumer’s income process. For instance, this shock could determine whether or not a consumer is employed or how many hours they can work in a given period. The agent’s can invest in a single-period, risk-free bond. Importantly, markets are not complete, so the agents cannot perfectly insure their risks. The consumer’s problem is then given by

It is assumed that consumers are all identical ex-ante, but because they receive different shocks to their income, they will be different ex-post. Utility is generally given by

Aiyagari uses this functional form with various values for

where

where

The consumers are assumed to be borrowing constrained. Aiyagari denotes this constraint by

Here

This is the maximum amount a consumer could payback given that they received a series of bad shocks. Because an agent could never guarantee that they could payback more than this amount, it is the most that will be lent to them. Thus, it is the “natural borrowing limit” and we impose that

Solving the Model

After all of that discussion on the borrowing limit, Aiyagari uses a transformation of the model to effectively remove the limit. Rather than using

and the state variable

We can think of

The consumer’s problem will now be written as

![\displaystyle E_0 \sum_t \beta^t\left[\frac{(z_t - \hat{a}_{t+1})^{1-\mu} - 1}{1-\mu} + \frac{\zeta}{3}\min\{\hat{a}_{t+1},0\}^3 \right]\\ \text{s.t. } z_t = w l_t + (1+r)\hat{a}_t - r\varphi,\ \forall t](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle+E_0+%5Csum_t+%5Cbeta%5Et%5Cleft%5B%5Cfrac%7B%28z_t+-+%5Chat%7Ba%7D_%7Bt%2B1%7D%29%5E%7B1-%5Cmu%7D+-+1%7D%7B1-%5Cmu%7D+%2B+%5Cfrac%7B%5Czeta%7D%7B3%7D%5Cmin%5C%7B%5Chat%7Ba%7D_%7Bt%2B1%7D%2C0%5C%7D%5E3+%5Cright%5D%5C%5C+%5Ctext%7Bs.t.+%7D+z_t+%3D+w+l_t+%2B+%281%2Br%29%5Chat%7Ba%7D_t+-+r%5Cvarphi%2C%5C+%5Cforall+t+&bg=ffffff&fg=73757D&s=0&c=20201002)

The term

Following Aiyagari, we will use the following parameters

# Model Primitives

β = 0.96

δ = 0.08

α = 0.36

μ = 5.0 # μ ∈ {1,3,5}

To solve this model we need a finite representation for the process

Tauchen’s Method

Tauchen (1986) proposed a method of approximating an

using Cubature

N = 7 # Number of grid points

m = 3 # Number of standard deviations

σ = 0.2 # σ ∈ {0.2, 0.4}

ρ = 0.6 # ρ ∈ {0.0, 0.3, 0.6, 0.9}

Σ = σ^2*sqrt(1-ρ^2)^2# Correlation Matrix

Σy = σ # Standard Deviation

ivΣ = 1/Σ

# Calculate Grid Values and Steps

maxy = m*Σy # Three standard deviations high

miny = -m*Σy # Three standard deviations low

ys = collect(linspace(miny, maxy, N)) # Vector of values

step = ys[end]/(N-1) # Step size

ys

7-element Array{Float64,1}:

-0.6

-0.4

-0.2

0.0

0.2

0.4

0.6

Next, we need to calculate the probability in each interval of our grid. Note that

# Calculate Markov Matrix

P = zeros(N, N);

for j = 1:N

μ = ρ*ys[j]

for l = 1:N

lowX = ys[l] - μ - step

l == 1 && (lowX = ys[l] - μ - step - 100.0)

highX = ys[l] - μ + step

l == N && (highX = ys[l] - μ + step + 100.0)

(val,err) = hcubature(x -> exp(-.5*x'*ivΣ*x)[1], lowX, highX,

reltol=1e-4, abstol=0, maxevals=0)

P[j,l] = (val ./ sqrt(2 *pi * Σ))

end

end

P = P ./ sum(P, 2)

0.467838 seconds (527.03 k allocations: 22.734 MB, 1.22% gc time)

7×7 Array{Float64,2}:

0.190787 0.455383 0.301749 … 0.0020016 1.84984e-5 3.82913e-8

0.0520813 0.301749 0.455383 0.0164242 0.000367205 1.87299e-6

0.00877448 0.12152 0.419444 0.0802333 0.00427914 5.33123e-5

0.000889025 0.0295073 0.235589 0.235589 0.0295073 0.000889025

5.33123e-5 0.00427914 0.0802333 0.419444 0.12152 0.00877448

1.87299e-6 0.000367205 0.0164242 … 0.455383 0.301749 0.0520813

3.82913e-8 1.84984e-5 0.0020016 0.301749 0.455383 0.190787

In the above code, I use the Cubature package to carry out the integration. You could also using Gauss-Hermite quadrature to evaluate this integral as well. The difference in run-time doesn’t matter when we use a coarse grid.

This defines the Markov transition matrix that approximates our original AR(1) process. This allows us to perform our calculations on a single continuous state variable (in this case capital) and one discrete state variable (the income process), which will lead to simpler calculations. Aiyagari renomalizes the income process so that the average amount of labor supplied is equal to

statdst = inv((eye(N) - P + ones(N,N))')*ones(N) El = dot(exp(ys)',statdst) L = exp(ys)/El

Finite Element Method

There are a number of different ways to solve for the consumer’s policy function. Probably the most commonly used are value function or policy iteration. Because those have been done elsewhere, I will use the Finite Element Method instead. I won’t go into the details of implementing the Finite Element Method here, but instead will only discuss its application to this problem. A more general treatment of the method can be found in Ellen McGrattan’s 1993 paper.

The first-order conditions of our approximate problem are given by

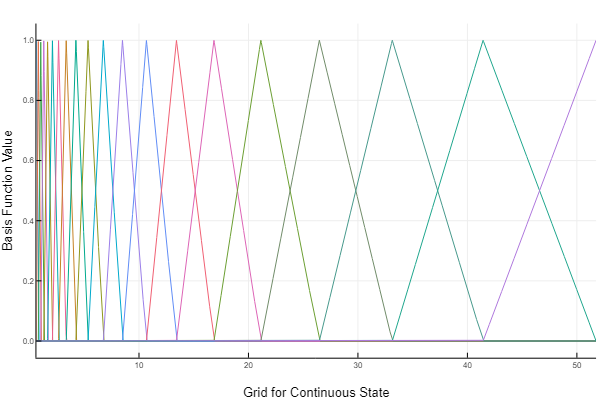

We want to approximate the optimal savings function using a piecewise linear function, that is

Here

Notice that they range from 0 to 1, and only two basis functions are non-zero between any two points on our grid (our grid points are located where the basis functions become zero). Also notice that our grid over the continuous state does not have to be evenly spaced. In this example, we have placed more points near 0 as this is where the kink is in the savings policy function. The coefficients for our linear approximation will be equal to the policy function at each point on our grid, and for points not falling on our grid, we will linearly approximate between the neighboring coefficients.

We need to choose values for the coefficients that generates a good approximation of our policy function, i.e. the average error in our Euler Equation will be small. To do this, I use the method of weighted residuals. Define the residual of the Euler Equation as

If we had the true policy function, this residual would be zero everywhere. We unfortunately do not have the true policy function, so we are going to try and minimize a special weighted integral of this residual equation. Specifically, we will choose our

where

As always, we start with a custom type which we will use to store the model parameters as well as the transition matrix, the grids, and the coefficients for our interpolation.

# Interpolating Object

type GalerkinObj

β::Float64

δ::Float64

α::Float64

ψ::Float64

μ::Float64

ϕ::Float64

w::Float64

r::Float64

ζ::Float64

P::Array{Float64, 2}

states::Array{Float64,1}

θs::Array{Float64, 2}

grid::Array{Float64, 1}

function GalerkinObj(β, δ, α, ψ, μ, ϕ, w, r, ζ, P, states, grid)

return new(β, δ, α, ψ, μ, ϕ, w, r, ζ, P, states, zeros(length(states), length(grid)), grid)

end

end

We now define a few helpful routines, taking advantage of Julia’s multiple dispatch. The first routine that we define simply takes an input

# Interpolate for specific state

function(itp::GalerkinObj)(k::Float64, s::Int)

g = itp.grid

k >= g[end] && return itp.θs[s, end] * k/g[end]

g[1] = g[end]) & (d == length(itp.grid)) && return k/g[end]

(g[1] = g[end] && return itp.θs[s, end] / g[end]

g[1] < k && return 0.0 #* k/g[1]

lb = searchsortedlast(itp.grid, k)

ub = lb + 1

return -itp.θs[s, lb] * 1.0/(g[ub] - g[lb]) + itp.θs[s,ub] * 1.0 /(g[ub] - g[lb])

end

To define the relevant grids, it helps to identify the minimum and maximum sustainable cash-in-hand. The minimum cash-in-hand that an agent can have is the lowest wage in the lowest productivity state. The lowest wage occurs when the highest interest rate occurs, which is equal to the time value of consumption. The largest sustainable cash-in-hand occurs when the capital stock is at its maximum sustainable value, i.e. when production perfectly offsets depreciation. I use these values as the lower and upper bound on my grid, and then use a nonlinear transformation to place more points near the origin.

lmin = L[1] # Implied minimum wage and cash on hand rT = 1/β-1 wmin = (1-α)*(α/(rT + δ))^(α/(1-α)) # L/K evaluated when r = rT zmin = wmin*lmin # Implied maximum capital and cash on hand kmax = δ^(1/((α-1))) zmax = kmax^α + (1-δ)*kmax # Initial guess for interest rate and wages rav = rT*0.72 wav = (1-α)*(α/(rav + δ))^(α/(1-α)) # Grid over cash-on-hand zGrid = convert(Array, collect(linspace(zmin^(1/50), zmax^(1/50), 20))).^50; # Maximum amount an agent can save is just the cash-in-hand maxa = zGrid'

Using these values, we initialize our custom type.

go = GalerkinObj(β, δ, α, ψ, μ, 0.0, wav, rav, 0.0, P, L, zGrid);

We need to translate the residual equation into a function. No surprises here, the below function is a direct translation of the residual equation into code.

function R_all(z::Float64, s::Int64, â::GalerkinObj)

β, δ, α, ψ, μ, ϕ, w, r, ζ, P = â.β, â.δ, â.α, â.ψ, â.μ, â.ϕ, â.w, â.r, â.ζ, â.P

l = â.states

â′ = â(z, s)

rhs = (z - â′ )^(-μ) - ζ * min(â′, ϕ)^2

lhs = 0.0

for j in eachindex( l )

z′s = w*l[j] + (1.0+r)*â′ - r*ϕ

lhs += (z′s - â(z′s, j))^-μ * P[s, j]

end

lhs = (1.0 + r)*β*lhs

return rhs - lhs

end

It will also be helpful to define the derivative of the residual equation with respect to an arbitrary coefficient $\alpha_{i,s}$ (in the below function, i = d and s = d2). We will be using Newton’s Method to solve the system of weighted residual equations, and so we will need to be able to calculate this derivative at arbitrary points. The only part below that is tricky is evaluating the derivative of

function R′_all(d::Int64, d2::Int64, z::Float64, s::Int64, â::GalerkinObj)

β, δ, α, ψ, μ, ϕ, w, r, ζ, P = â.β, â.δ, â.α, â.ψ, â.μ, â.ϕ, â.w, â.r, â.ζ, â.P

â_d = â(d, z, d2)

l = â.states

â′ = â(z, s)

rhs = μ*(z - â′ )^(-μ-1.0)*â_d*(d2==s) - ζ * 2.0 * min(â′, ϕ)*â_d*(d2==s)

lhs = 0.0

if d2 == s

for j in eachindex( l )

z′s = w*l[j] + (1.0+r)*â′ - r*ϕ

lhs += -μ*(z′s - â(z′s, j))^(-μ-1.0)*((1.0+r)*(â_d - â(z′s, j, 1)*â_d) - â(d, z′s, j)*(s==j)) * P[s, j]

end

else

z′s = w*l[d2] + (1.0+r)*â′ - r*ϕ

lhs = -μ*(z′s - â(z′s, d2))^(-μ-1.0)*( - â(d, z′s, d2) ) * P[s, d2]

end

lhs = (1.0 + r)*β*lhs

return rhs - lhs

end

This last function we need calculates the weighted residual equations and then uses Newton’s Method to set the system of equations as close to zero as possible. I set the tolerance to

function weightedResidual(go::GalerkinObj, N::Int64)

nodes, weights = gausslegendre(N)

rescl = zeros(length(nodes))

Gθ = zeros(length(go.θs), length(go.θs))

res = zeros(length(go.θs))

g = vcat([go.grid[1]], go.grid, [go.grid[end]])

eps = vec(go.θs)

count = 1

while (maximum(abs(eps)) > 1e-5)*(100 > count)

count += 1

# Reset Values to zero

for i = 1:length(res)

res[i] = 0.0

for j = 1:length(res)

Gθ[i,j] = 0.0

end

end

for i = 3:length(g)

for j = 1:length(nodes)

rescl[j] = (nodes[j] + 1.0)*(g[i]-g[i-2])/2.0 + g[i-2]

end

for s = 1:length(go.states)

idx1 = length(go.states)*(i-3) + s

for j = 1:length(rescl)

newweight = ifelse( g[i-1] < rescl[j],

(rescl[j] - g[i-2])/(g[i-1] - g[i-2]) ,

(g[i] - rescl[j])/(g[i] - g[i-1])

) * weights[j] * (g[i]-g[i-2])/2.0

res[idx1] += R_all(rescl[j], s, go) * newweight

for gs = 1:length(go.states)

for gp = 1:length(go.grid)

idx2 = length(go.states)*(gp-1) + gs

Gθ[idx1, idx2] += R′_all(gp, gs, rescl[j], s, go) * newweight

end

end

end

end

end

eps = -Gθ\res

for i = 1:length(go.θs)

go.θs[i] += eps[i]

end

end

@show maximum(abs(eps))

return nothing

end

I set

go.ζ = 100000.0 go.θs = maxa*0.97.*ones(ys); @time weightedResidual(go, 9)

maximum(abs(eps)) = 2.802889423022742e-6 3.282654 seconds (483 allocations: 8.643 MB, 0.14% gc time)

The policy function generated by this code is identical to that reported in Aiyagari 1993.

Calculating the Stationary Distribution

The final step in solving the Aiyagari model is calculating the stationary distribution. Finding the stationary distribution involves solving for the interest rate and wage such that next periods average capital is the same as the current periods. The first hurdle is solving for the average capital holdings given a fixed interest rate. Aiyagari used the fact that the capital distribution is ergodic and calculated the average asset holdings from a long time series for a single agent. In subsequent studies, researchers have instead simulated short time series for many agents and then calculated average asset holdings across all agents in the last few periods. Both of these methods work and are fairly robust, however they aren’t very efficient. Young (2010) proposed discretizing the asset distribution and then calculating a transition matrix for this discrete distribution using the known transition probabilities and the agent’s policy function. Violante has a good discussion of this method in his course notes here.

The function below takes our policy function object

where

function calcStatDist(â::GalerkinObj, agrid)

P = â.P

r3 = â.r

w3 = â.w

Φ = zeros(size(P,1)*length(agrid), size(P,1)*length(agrid));

AM = size(Φ,1)

M = length(agrid)

for i = 1:AM

k = div(i-1, M) + 1

a1 = ifelse(mod(i, M) == 0, M, mod(i, M))

a′ = â(agrid[a1]*(1+r3) + w3*L[k], k)

indxL = searchsortedlast(agrid, a′)

indxH = indxL + 1

w1 = (agrid[indxH] - a′)/(agrid[indxH] - agrid[indxL])

w2 = (a′ - agrid[indxL])/(agrid[indxH] - agrid[indxL])

for j = 1:size(P,1)

Φ[i,M*(j-1) + indxL] = P[k, j] * w1

Φ[i,M*(j-1) + indxH] = P[k, j] * w2

end

end

Φ = Φ./sum(Φ,2);

statDist = (eye(M*size(P,1)) - Φ + ones(M*size(P,1),M*size(P,1)))'\ones(M*size(P,1))

dot(statDist, repeat(agrid, outer = size(P,1)))::Float64

end

Once we have determined our average capital, we need to search over values of

To find the correct interest rate, we will compare the average capital implied by our transition matrix and compare it to the capital that generates our current guess of

If our policy function generates average holdings above this, we know that the interest rate is too high, i.e. agents are over-investing, and we adjust it downwards. If our policy function generates a lower capital stock then agents are under-investing and we adjust the interest rate upwards. The bisection method continuously updates the lower and upper bounds of our interest rate depending on whether our previous guess was too low or two high and will eventually converge to the stationary interest rate.

function bisection(go::GalerkinObj, agrid::Array{Float64,1})

α = go.α

δ = go.δ

rT = 1.0 - 1.0\go.β

r3 = rT*0.72 # Initial Guess

r2 = rT # Upper bound

r1 = 0.0 # Lower Bound

eps = 1.0; count = 0

while(eps > 1e-5)*(5 > count)

rtmp = (r1 + r2)/2

eps = abs(rtmp - r3)

r3 = deepcopy(rtmp)

@show eps

w3 = (1-α)*(α/(r3 + δ))^(α/(1-α))

maxa = max((1+r3)*zGrid' .+ w3*L,0)

newP2 = findRoot(vec(αs2), r3, w3)

αs2 = reshape(newP2, size(L,1), length(zGrid))

â = GalerkinObj(αs2, zGrid);

stD, as = calcStatDist(â, P, r3, w3, Max = 200.0, N = 500)

agrid = collect(linspace(-0.1, 200, 500));

a′ = vcat([â(a)' for a in agrid]...);

e = (1.0 - ψ*((1+r3)*agrid .- a′)./(L'*w3))/(1+ψ);

tmp = reshape(stD, Int(length(stD)/size(P,1)), size(P,1))

Lss = sum(tmp.*e)

K3 = ((r3+δ)/α)^(-1/(1-α))*Lss

as > K3 && (r2 = r3)

K3 > as && (r1 = r3)

count += 1

end

return nothing

end

@time bisection(go, agrid)

maximum(abs(eps)) = 3.809819676979794e-6 maximum(abs(eps)) = 8.95310406449911e-6 maximum(abs(eps)) = 3.7637412435255835e-8 maximum(abs(eps)) = 8.684272846885449e-8 maximum(abs(eps)) = 4.667653538520587e-6 maximum(abs(eps)) = 5.434474939187872e-8 maximum(abs(eps)) = 3.933242153661582e-9 maximum(abs(eps)) = 2.4705718111657407e-10 maximum(abs(eps)) = 3.95137873051283e-6 maximum(abs(eps)) = 9.838429366693355e-7 maximum(abs(eps)) = 2.457911398865253e-7 maximum(abs(eps)) = 6.146862346294397e-8 44.151404 seconds (621.98 k allocations: 8.789 GB, 16.62% gc time)

The resulting interest rate for capital is very close to what Aiyagari originally calculated (see Table II in Aiyagari (1994) for the case when

go.r

0.035986328125000036

References

- S. Rao Aiyagari, 1994. “Uninsured Idiosyncratic Risk and Aggregate Saving,” The Quarterly Journal of Economics, Oxford University Press, vol. 109(3), pages 659-684.

- Ellen R. McGrattan, 1993. “Solving the stochastic growth model with a finite element method,” Staff Report 164, Federal Reserve Bank of Minneapolis.

- Young, Eric R., 2010. “Solving the incomplete markets model with aggregate uncertainty using the Krusell-Smith algorithm and non-stochastic simulations,” Journal of Economic Dynamics and Control, Elsevier, vol. 34(1), pages 36-41, January.