Traditional models with default risk predict that the incentive to default increases with the agent’s income. This is true in the models of Kehoe and Levine (1993), Kocherlakota (1996), and Alvarez and Jermann (2000). The idea is that the cost of being excluded from financial markets is low when income is high, lowering the penalty associated with defaulting. This result runs counter to the historical record, however, as we generally see delinquency rates increase during recessions (e.g. see 2007 Credit Card Delinquency Rates) and sovereign defaults occur following negative shocks (e.g. the Greek debt crisis). To me, this is more intuitive as we would anticipate that defaults should increase when it becomes more difficult to rollover your current debt. One model that captures this dynamic is the Arellano model of sovereign default. Unlike models with complete contracts, it is able to generate default in equilibrium and interest rate spreads that are counter-cyclical. While the model and its implications are very interesting, the purpose of this write-up is not to discuss the economics but to review the computational details in solving such a model and to use this model to demonstrate various aspects of adaptive sparse grids.

As a brief aside, I have found that blocks of the text and code below mysteriously disappear when updating the page. If any parts of the below code do not work, just shoot me an email and I will update it.

Model Overview

The model considers a small open endowment economy with a representative consumer who has the following utility function

The economy’s income follows an

where

where

Because default is endogenous,

After a default, two things happen. First, the country is excluded from financial markets. Therefore it will not be able to borrow or lend money and must consume its endowment. However, the country will be able to re-enter financial markets with an exogenous probability

![\bar{y} = 0.969 E[y]](https://s0.wp.com/latex.php?latex=%5Cbar%7By%7D+%3D+0.969+E%5By%5D&bg=ffffff&fg=73757D&s=0&c=20201002)

The recursive equilibrium will be characterized by three value functions and their associated policy functions. The value function for default is given by

The value function for continuing payment is given by

and the government’s value function is given by the maximum of these two

Default occurs when

where we define

β = 0.953 # Discount Factor σ = 2.0 # Risk coefficient r = 0.017 # Risk free interest rate ρ = 0.945 # Income persistence η = 0.025 # Income variance θ = 0.282 # Probability of Re-entry

Discrete Approximation

In her original paper, Arellano solved this model by discretizing the state space and then looping over the grid points to find the optimal level of bond holdings given an initial level of debt and an income shock. With a discretized state-space, value and policy functions can be replaced with vectors and our contraction mapping will converge to a fixed point in a finite number of iterations. It is an exact solution to an approximate questions. However, this method requires us to make few choices. First, we need to define a grid over

Tauchen’s Method

Tauchen (1986) proposed a method of approximating an

using Cubature N = 21 # Number of grid points m = 3 # Number of standard deviations Σ = η^2# Correlation Matrix Σy = η/sqrt(1-ρ^2) # Standard Deviation ivΣ = 1/Σ # Calculate Grid Values and Steps maxy = m*Σy # Three standard deviations high miny = -m*Σy # Three standard deviations low ys = collect(linspace(miny, maxy, N)) # Vector of values step = ys[end]/(N-1) # Step size

Because

The PDF for

# Calculate Markov Matrix

P = zeros(N, N);

for j = 1:N

μ = ρ*ys[j]

for l = 1:N

lowX = ys[l] - μ - step

l == 1 && (lowX = ys[l] - μ - step - 100.0)

highX = ys[l] - μ + step

l == N && (highX = ys[l] - μ + step + 100.0)

(val,err) = hcubature(x -> exp(-.5*x'*ivΣ*x)[1], lowX, highX,

reltol=1e-4, abstol=0, maxevals=0)

P[j,l] = (val ./ sqrt(2 *pi * Σ))

end

end

P = P ./ sum(P, 2);

statdst = inv((eye(N) - P + ones(N,N))')*ones(N)

Ey = dot(exp(ys)',statdst)

ŷ = 0.969 * Ey

Value Function Iteration

First, we will construct a custom type that will hold all of our model parameters as well as the value functions and policy functions. This just improves our run time by not ensuring type stability and reusing all arrays (including temporary arrays).

type ValFunc

β::Float64

σ::Float64

r::Float64

θ::Float64

ŷ::Float64

ys::Array{Float64,1}

P::Array{Float64, 2}

Bs::Array{Float64,1}

Vd::Array{Float64,1}

Vc::Array{Float64,2}

Bpol::Array{Int64,2}

V::Array{Float64,2}

Vdtmp::Array{Float64,1}

Vctmp::Array{Float64,2}

δpol::Array{Float64,2}

function ValFunc(β, σ, r, θ, ŷ, ys, P, Bs)

return new(

β, σ, r, θ, ŷ, ys, P, Bs, zeros(length(ys)), zeros(length(ys), length(Bs)),

zeros(length(ys), length(Bs)), zeros(length(ys), length(Bs)), zeros(length(ys)),

zeros(length(ys), length(Bs)), zeros(length(ys), length(Bs))

)

end

end

Using our calculated transition matrix and our grids over

Bs = collect(linspace(-.45, .45, 201)); vf = ValFunc(β, σ, r, θ, ŷ, exp(ys)[:], P, Bs);

Next, lets calculate a generic utility function and autarky income function. Note that the argument “val” is a union of two custom types: “ValFunc” and “modelprimitives”. The latter is defined below for the continuous case.

function u( c::Float64, val::Union{ValFunc,modelprimitives} )

return c^(1.0-val.σ)/(1.0-val.σ)

end

function h(y::Float64, val::Union{ValFunc,modelprimitives} )

return min(y, val.ŷ)

end

Here is the bulk of the code. This actually does the value function iteration. Departing from Arellano’s original solution method, I use the one loop method that is recommended in the literature where default probabilities are updated in each iteration, rather than have an inner loop for the value functions and an outer loop for the default probabilities. For a more detailed discussion on the discrete solution method, the reader can check out the QuantEcon page on this model (here).

function update!(val::ValFunc)

eps = 1.0

iter = 0

ind0 = Int(floor(length(val.Bs)/2))

while (eps > 1e-4)*(1000 > iter)

for i = 1:length(val.ys) # Value of Default

expt = 0.0

for s = 1:length(val.ys)

expt += val.P[i, s] * ( val.θ * val.V[s, ind0] + (1-val.θ)*val.Vd[s] )

end

val.Vdtmp[i] = u( h(val.ys[i], val), val) + val.β*expt

end

for i = 1:length(val.ys) # Value of continuing payments

for b = 1:length(val.Bs)

val.Vctmp[i, b] = -Inf

for b′ = 1:length(val.Bs)

expt = 0.0

for s = 1:length(val.ys)

expt += val.P[i, s] * val.V[s, b′]

end

curr = u( max(val.ys[i] - (1.0-val.δpol[i, b′])/(1+val.r)*val.Bs[b′] + val.Bs[b], 0), val) + val.β*expt

if curr > val.Vctmp[i, b]

val.Vctmp[i, b] = curr

val.Bpol[i, b] = b′

end

end

end

end

err = 0.0

# Update Value Functions

for i = 1:length(val.ys)

for b = 1:length(val.Bs)

val.V[i,b] = max(val.Vdtmp[i], val.Vctmp[i,b])

err = max(err, abs(val.Vd[i] - val.Vdtmp[i]), abs(val.Vc[i, b] - val.Vctmp[i, b]))

val.Vd[i] = val.Vdtmp[i]

val.Vc[i, b] = val.Vctmp[i, b]

end

end

# Update Default Probabilities

for i = 1:length(val.ys)

for b = 1:length(val.Bs)

val.δpol[i,b] = 0.0

for j = 1:length(val.ys)

if val.Vc[j,b] < val.Vd[j]

val.δpol[i,b] += val.P[i, j]

end

end

end

end

eps = err

iter += 1

end

@show eps

end

@time vf = ValFunc(β, σ, r, θ, ŷ, exp(ys)[:], P, Bs); @time update!(vf)

0.000117 seconds (22 allocations: 199.766 KB) eps = 9.937995512387943e-5 14.008138 seconds (59.51 k allocations: 2.163 MB)

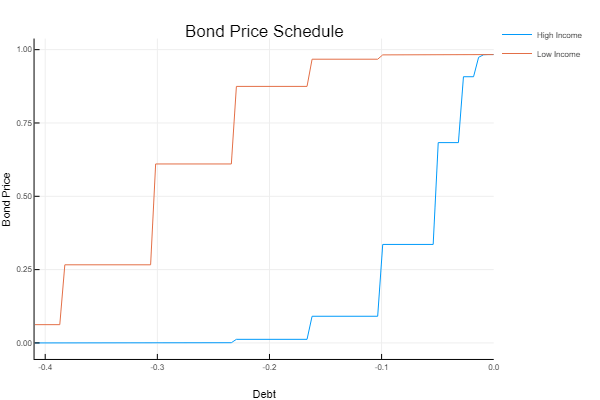

This code faithfully recreates Arellano’s Figure 3. We can see that it is more costly to borrow when bond holding are very low and approaches the risk free rate when bond holdings are high.

using Plots tot = (1.0-vf.δpol)/(1.0 + vf.r) plot(Bs[10:101], [tot[11,10:101], tot[14,10:101]], label = ["High" "Low"], xlabel = "B", ylabel = "q")

Continuous Approximation

The discrete solution method paved over a few difficulties in solving this model. First, integrating the default probabilities was reduced to summing probabilities over a finite number of states. Similarly, finding the optimal level of bond holdings was reduced to checking all possible levels and selecting he maximum one, a process that is not feasible with continuous states. Finally, our value function will have a kink in it, meaning we will want to concentrate grid points around the kink for a better approximation. However, the location of the kink will change at each stage of the value function iteration, necessitating we either specify a fine grid or choose our grid endogenously. Adaptive sparse grids provide a solution to each of these problems. The adaptivity only places grids at points where our interpolation approximation is poor, meaning that they can approximate kinked functions closely without adding unnecessary points. The simple linear basis functions make integration and differentiation straightforward, so we can use the built in differentiation to employ a bisection search to find the optimal level of bond holdings and use the built in integration to calculate the default probabilities.

It should be noted that using continuous methods to solve this model is not merely an academic exercise. Martinez et. al. (2010) found that the results in Aguiar and Gopinath (2006) and Arellano (2008) could be sensitive to the discretization that they use. It is therefore important that researchers have methods of solving these models that don’t rely on discretization.

I have stored the adaptive sparse grid code used to solve this model here.

include("[filepath]/AdaptiveSparseGrid/fastasgd.jl")

using fastasgd

using FastGaussQuadrature

d = 2 # Number of Dimesions (2 because we are solving over income (y) and debt (B)) states = 1 # Number of discrete states (none) ord = 11 # Maximum depth of approximation # Bounds for B and y lb = [-0.45, exp(ys)[1]] ub = [0.45, exp(ys)[end]] # Interpolation Objects V_ = ASG(d, states, ord, lb, ub); V_t = ASG(d, states, 18, lb, ub); δ_ = ASG(d, states, ord, lb, ub); Vd = ASG(1, states, ord, [lb[2]], [ub[2]]); Vdt = ASG(1, states, ord, [lb[2]], [ub[2]]); Vc = ASG(d, states, ord, lb, ub); δt = ASG(1, 1, 14, [lb[2]-0.1], [ub[2]+0.1]); # Initialize Values for Interpolation Objects @time adaptivegrid( V_, x -> 0.0, 0.0001, 0.01, 1); @time adaptivegrid( δ_, x -> 1.0, 0.0001, 0.01, 1); @time adaptivegrid( Vd, x -> 0.0, 0.0001, 0.01, 1); @time adaptivegrid( Vc, x -> 0.0, 0.0001, 0.01, 1);

We will frequently be evaluating expectations such as

# Gauss-Hermite for Apporximation Integral nodes, weights = gausshermite(4); weights = weights / sqrt(π);

To ensure type stability, I create another custom type to store all of the model parameters as well as the nodes and weights for quadrature.

type modelprimitives

β::Float64

σ::Float64

r::Float64

θ::Float64

ŷ::Float64

ρ::Float64

η::Float64

nodes::Array{Float64, 1}

weights::Array{Float64, 1}

function modelprimitives(β, σ, r, θ, ŷ, ρ, η, nodes, weights)

return new(

β, σ, r, θ, ŷ, ρ, η, nodes, weights

)

end

end

mp = modelprimitives(β, σ, r, θ, ŷ, ρ, η, nodes, weights);

Solving for Optimal Bond Holdings

The first step is to define the mapping for the value of default. This function is fairly simple as there is no optimum to solve for. We take the current guess for

function TVd(y::Float64, V::ASG, Vd::ASG, mp::modelprimitives )

expt = 0.0

for s = 1:length(mp.nodes)

y′ = exp(sqrt(2.0)*mp.η*mp.nodes[s] + mp.ρ*log(y))

expt += mp.weights[s] * (mp.θ * V(0.0, y′, 1) + (1.0 - mp.θ)*Vd(y′, 1) )

end

return u( h( y, mp ), mp) + mp.β*expt

end

Next, we need to update the value function given that the government continues servicing its debt. To do this, we need a guess for the value function

![[-0.45, 0.45]](https://s0.wp.com/latex.php?latex=%5B-0.45%2C+0.45%5D&bg=ffffff&fg=73757D&s=0&c=20201002)

This code is the derivative of the contraction operator with respect to

function TVc′(y::Float64, B::Float64, B′::Float64, V::ASG, δ::ASG, mp::modelprimitives )

expt = 0.0

for s = 1:length(mp.nodes)

y′ = exp(sqrt(2.0)*mp.η*mp.nodes[s] + mp.ρ*log(y))

expt += mp.weights[s] * V(1, B′, y′, 1)

end

c = y - (1.0 - δ(B′, y, 1))/(1.0 + mp.r)*B′ + B

return max(c, 0.0)^(-mp.σ)*(-(1.0 - δ(B′, y, 1))/(1.0 + mp.r) + δ(1, B′, y, 1)/(1.0 + mp.r)*B′ ) + mp.β*expt

end

Here is the bisection method to solve for the maximum.

function TVc(y::Float64, B::Float64, V::ASG, δ::ASG, mp::modelprimitives )

B′L = V.lb[1]

B′H = V.ub[1]-0.001

eps = 1.0

count = 0

B′ = B′H

f1 = 0.0

while (eps > 1e-8)*(count = 0.0 )

eps = abs(B′ - (B′L + B′H)/2.0)

B′ = (B′L + B′H)/2.0

f1 = TVc′(y, B, B′, V, δ, mp )

if 0.0 <= f1

B′L = B′

elseif f1 < 0.0

B′H = B′

else

break

end

count += 1

end

abs(B′ - V.lb[1]) < 1e-3 && (B′ = V.lb[1])

expt = 0.0

# Using quadrature for the expectation

for s = 1:length(mp.nodes)

y′ = exp(sqrt(2.0)*mp.η*mp.nodes[s] + mp.ρ*log(y))

expt += mp.weights[s] * V(B′, y′, 1)

end

c = y - (1.0 - δ(B′, y, 1))/(1.0 + mp.r)*B′ + B

return u( max(c, 0.0), mp) + mp.β*expt

end

Integrating the Default Probabilities

The default probabilities are merely the integral of the PDF for the income process over the default set. Note that in general the default set could be made up of disjoint subsets, so this integral is not trivial to approximate. To overcome this difficulty, I use adaptive sparse grids to approximate the PDF over the area where

function solδ(B::Float64, y::Float64, δt::ASG, Vc::ASG, Vd::ASG)

adaptivegrid( δt, x -> ifelse(Vd(x[1], 1) > Vc(B, x[1], 1), 1.0/sqrt(2.0*pi*mp.η^2)*exp(-(log(x[1])-mp.ρ*log(y))^2/(2*mp.η^2))/x[1], 0.0), 0.0001, -0.00001, 1);

u1 = deepcopy(δt.ub)

return min(iinterpolate(u1, δt, δt.l, 1), 1.0)

end

Value Function Iteration

We can combine the above pieces of code into a contraction. Here I only use 15 iterations, which gives a fairly close approximation. I am still working on a good metric for checking the convergence of a contraction with adaptive sparse grids. There are many approximations that give very close answers but have different points with non-zero hierarchical surpluses, making a comparison of the hierarchical surpluses a poor approximation of the contraction error. One possibility is using Gauss-Legendre quadrature to approximate the average error to the Euler Equation, but I have not found a great implementation yet. The code is not very fast, mainly because I use low pruning coefficients. The speed can be increased by loosening the pruning coefficients and using a more robust solver than the bisection method.

@time for i = 1:15

adaptivegrid( Vc, x -> TVc(x[2], x[1], V_, δ_, mp), 0.01, 0.001, 1);

adaptivegrid( Vd, x -> TVd(x[1], V_, Vdt, mp), 0.01, 0.001, 1);

adaptivegrid( V_, x -> max(Vd(x[2],1), Vc(x[1], x[2], 1)), 0.001, 0.00001, 1);

Vdt = deepcopy(Vd)

adaptivegrid( δ_, x -> solδ(x[1], x[2], δt, Vc, Vd), 0.001, 0.00001, 1);

@show Vc(-0.4, 1.0,1) - Vd(1.0,1)

end

262.525034 seconds (931.77 M allocations: 38.152 GB, 2.87% gc time)

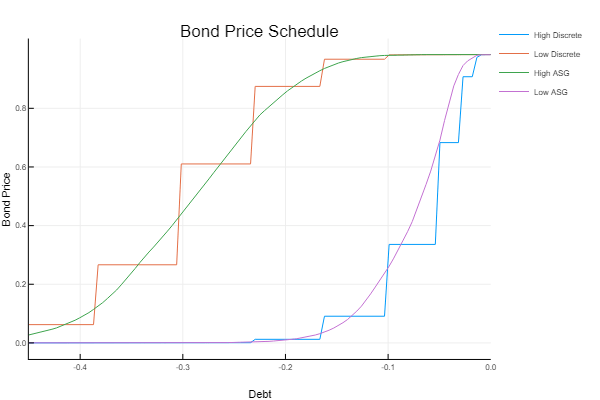

The below figure compares the continuous solution with Arellano’s original solution, showing that they are very similar. We can see that the bond price increases with bond holdings. Remember that you must pay

This figure recreates Arellano’s Figure 2, for the calibrated model. The default set is empty in the high state around

![[-0.23, -0.1]](https://s0.wp.com/latex.php?latex=%5B-0.23%2C+-0.1%5D&bg=ffffff&fg=73757D&s=0&c=20201002)

![[-0.05,-0.01]](https://s0.wp.com/latex.php?latex=%5B-0.05%2C-0.01%5D&bg=ffffff&fg=73757D&s=0&c=20201002)

References

- Arellano, Cristina. 2008. “Default Risk and Income Fluctuations in Emerging Economies.” American Economic Review, 98 (3): 690-712.

- Hatchondo, Juan Carlos and Martinez, Leonardo and Sapriza, Horacio, Quantitative Properties of Sovereign Default Models: Solution Methods Matter (April 2010). IMF Working Papers, Vol. , pp. 1-28, 2010.

- Tauchen, George, 1986. “Finite state markov-chain approximations to univariate and vector autoregressions,” Economics Letters, Elsevier, vol. 20(2), pages 177-181.

linspace , eye(N) and type were depreciated in Julia’s new systax

LikeLike